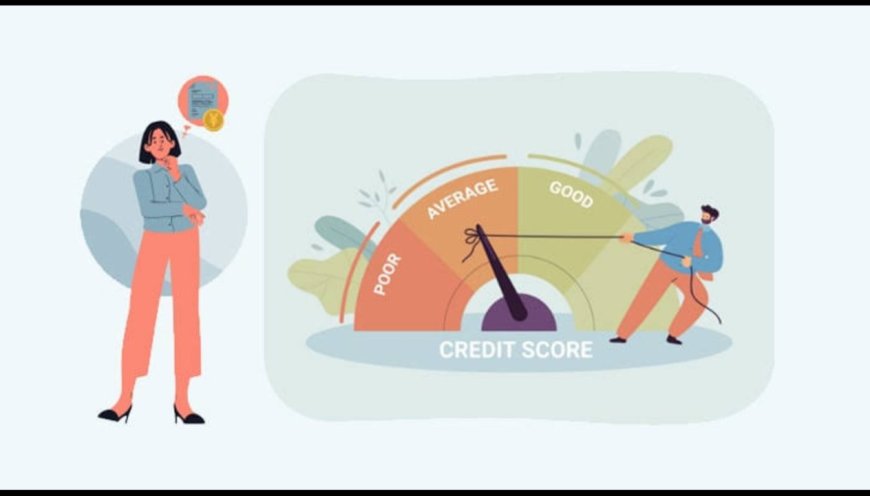

What are the general guidelines for the credit scores range?

Three digits make up a credit score. Typically, it uses a scale from 300 to 850. It predicts your likelihood of repaying loans and making payments on your obligations. Credit scores are likely to use data from your credit accounts. Credit reporting companies, commonly known as credit bureaus, collect such information and integrate it into your credit reports. Equifax, Experian, and TransUnion are the top three bureaus in terms of size. There isn't much of a difference between a "perfect" score and an excellent score. When it comes to the rates you can qualify for, the highest credit score you can earn is 850. In other words, don't worry about attempting to get an 850 credit scores range since scores constantly change

Guidelines for credit scores range

Creditors determine their own criteria for what ratings they will accept. But here are the general guidelines, which are as follows:

· We generally consider a credit score of 720 or greater to be an excellent score.

· Good credit scores range from 690 to 719.

· Fair credit scores range from 630 to 689.

· Poor credit also refers to scores of 629 or less.

In addition to your credit score, there are some additional variables. It includes your income and other debts. These elements might have an impact on your creditors' decision to approve or reject your application.

The FICO and VantageScore

Two businesses dominate credit scoring. Most people are familiar with the FICO score. The VantageScore is its main rival. They both typically work with a credit scores range of between 300 and 850. Additionally, each business has various variations of its grading system. The most commonly utilized scoring algorithms are VantageScore 3.0 and FICO 8.

Both VantageScore and FICO use the same data but weight it significantly differently. They frequently go together. If your VantageScore is outstanding, your FICO is probably also excellent. A score is a snapshot, and each time you look at it, the number may change. Your score may differ based on the credit bureau. They provided the information needed to construct it, as well as the timing of its supply. Each bureau's credit report is different since not all creditors report account activity to them.

The average credit score

Between the two main scoring methodologies, the typical credit score in the US differs a little. As of August 2022, the average FICO 8 score was 716, staying flat from the previous year. By the second quarter of 2021, the average VantageScore 3.0 score was 695.

Factors affecting your credit scores

FICO and VantageScore, the two main credit scoring algorithms, examine many of the same characteristics but weight them differently. The two factors that matter the most for both scoring models are:

1. On-time payment of bills

A slip-up here might cost you. A late payment that is 30 days or more past the due date remains on your credit report for years.

2. The amount you owe

Credit usage, or how much of your available credit you are utilizing, is almost as important as making on-time payments. It's advisable to use no more than 30% of your available credit; lower is preferable. There are various actions you can take to reduce your credit usage. This factor has a quick effect on scores.

Much less weight goes to these elements, although they are still important to consider:

· Credit age

Your credit score will improve the longer you've had credit and the older your accounts are on average.

· Credit mix

Scores incentivize having more than one sort of credit, such as a regular loan and a credit card.

· Applying for credit

When you make a credit application, a hard query on your credit report could cause a brief drop in your score.

Factors not affecting your credit scores

Some factors have no impact when calculating credit scores. However, these aspects primarily relate to demographic traits.

For instance, the estimate does not take into account your age, marital status, gender, race, or ethnicity. Neither is where you live nor your previous employment history, which may include details like your pay, title, or company.

Final Verdict

You can check your credit scores range report on your own. This wouldn't harm your score to see what the lender is likely to find. A personal finance website provides a TransUnion VantageScore of 3.0. This allows you to obtain a free credit score. Using the same score each time you check is crucial. Any other approach is equivalent to trying to keep track of your weight while using various scales. Perhaps alternate between pounds and kilogrammes. So choose a score and develop a strategy to keep an eye on your credit. One score's changes will probably show up in the others as well.

Keep in mind that grades might change, just like weight. These variations won't have an effect on your financial security as long as you keep it within a healthy range. By putting your credit on hold, you may defend your credit. You can still use credit cards, but no one can apply for credit using your personal information. It is for this reason that no one has access when your credit is frozen.

What's Your Reaction?